Advice on how to reassure and inform your debt management clients

Debt can be a terrifying, intimidating time for your clients. When they come to you, it is because they have exhausted every possible option and they are in desperate need of financial assistance. At this time they are likely feeling a loss of control, which is compounded by the fact that they have so many unanswered questions. They will likely have heard misleading debt myths and terrifying tales, so it is up to you, as the professional, to set them straight, comfort them and help them see clearly.

Debt resolution is generally a restrictive and challenging process. For those applying for an Individual Voluntary Agreement (IVA), Debt Management Plan (DMP) or bankruptcy, they will have to abide by certain restrictions and budgets. However, they might have exacerbated the situation in their own minds. As professionals, we know debt and its implications intimately, and as such we might have lost touch with certain queries or concerns that dominate the minds of your clients.

In order to assist people effectively and professionally, we have outlined the most pressing queries that your clients may want to ask, but are perhaps too intimidated to voice.

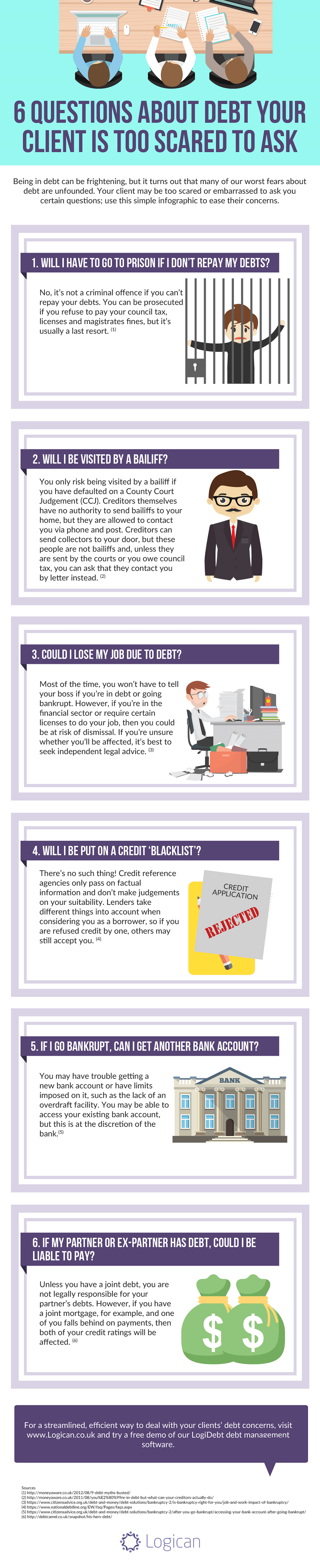

1. Am I going to go to prison?

This is not a stress that your client should have to bear on top of everything else, but it is likely that they consider prison a possibility at this point. Go to the effort of putting them at ease and explain that certain debts, including non-repayment of council tax, licenses and magistrates fines, may result in prosecution, but this is the last resort and unlikely to occur. The important thing is to focus on is repaying those debts; this is ultimately what everyone involved wants, and this is unlikely to happen if your client is in prison.

2. Will bailiffs be knocking at my door?

As the area of debt is unlikely to be a topic of expertise for your client, they probably don’t know that creditors have no authority to send bailiffs to their home — though they are able to contact them via telephone or post. Explain to your client that they will only be visited by bailiffs on certain, rare occasions, such as if they have defaulted on a County Court Judgement.

3. Will my boss find out about my debt?

This is a seriously worrying proposition for anyone already experiencing debt. Losing their capacity to make money in order to repay existing debt, should their boss find out about their financial situation, is a situation capable of causing a high degree of anxiety and depression.

Let your client know that, in most cases, there is no need to inform their boss of their IVA, DMP or bankruptcy. They are unlikely to find out unless they specifically perform a search on a relevant online database. The only time the issue of your clients’ debt raises concerns is if your client works in the financial sector or requires certain licenses to perform their job.

4. Will I be on a credit blacklist?

The ongoing myth of the infamous credit blacklist is one that perseveres and shows no sign of abating. It will do your client well to be informed that there is no such thing as a credit blacklist.

While credit reference agencies pass on information regarding your client’s current financial situation, this doesn’t mean that credit will be impossible to obtain. Every single lender bases its decision to give credit on select criteria. So while one creditor might decide against your client as a candidate based on their current circumstances, another lender might accept their application.

5. Will I be able to hold a bank account?

A bank account is necessary in this digital day and age, so your client needs to be informed in this area. Explain that while they are likely to be able to get a very basic bank account, there will be restrictions placed upon it. This will include, for obvious reasons, a lack of an overdraft.

6. Am I responsible for my partner’s (or ex-partner’s) debt?

If a client is swimming in debt, they will naturally want to be reassured that they will not be held responsible for debts that they didn’t even accumulate. Explain that unless the debt in question was obtained jointly, under both names, then they are not legally responsible for the debt. They will want to know about joint loans such as mortgages, where if one person falls behind in payments, they will both be responsible and both credit ratings will be affected.

Regardless of industry, all clients feel better and more at ease when they are more familiar with the process and how certain factors will affect them. Take the time to answer any and all questions, explain every step in detail and talk about your role in the matter.

You might want to talk to your client about the measures you have in place to assist the process, such as your insolvency software, which helps streamline and facilitate the repayment of your client’s debt. Remember at all times that your client is going through a testing period, and the better informed they are in general, the more prepared they will be.

This infographic was brought to you by Logican Solutions. Please feel free to add this infographic to your own website by copying and pasting the following embed code onto a page or post: